|

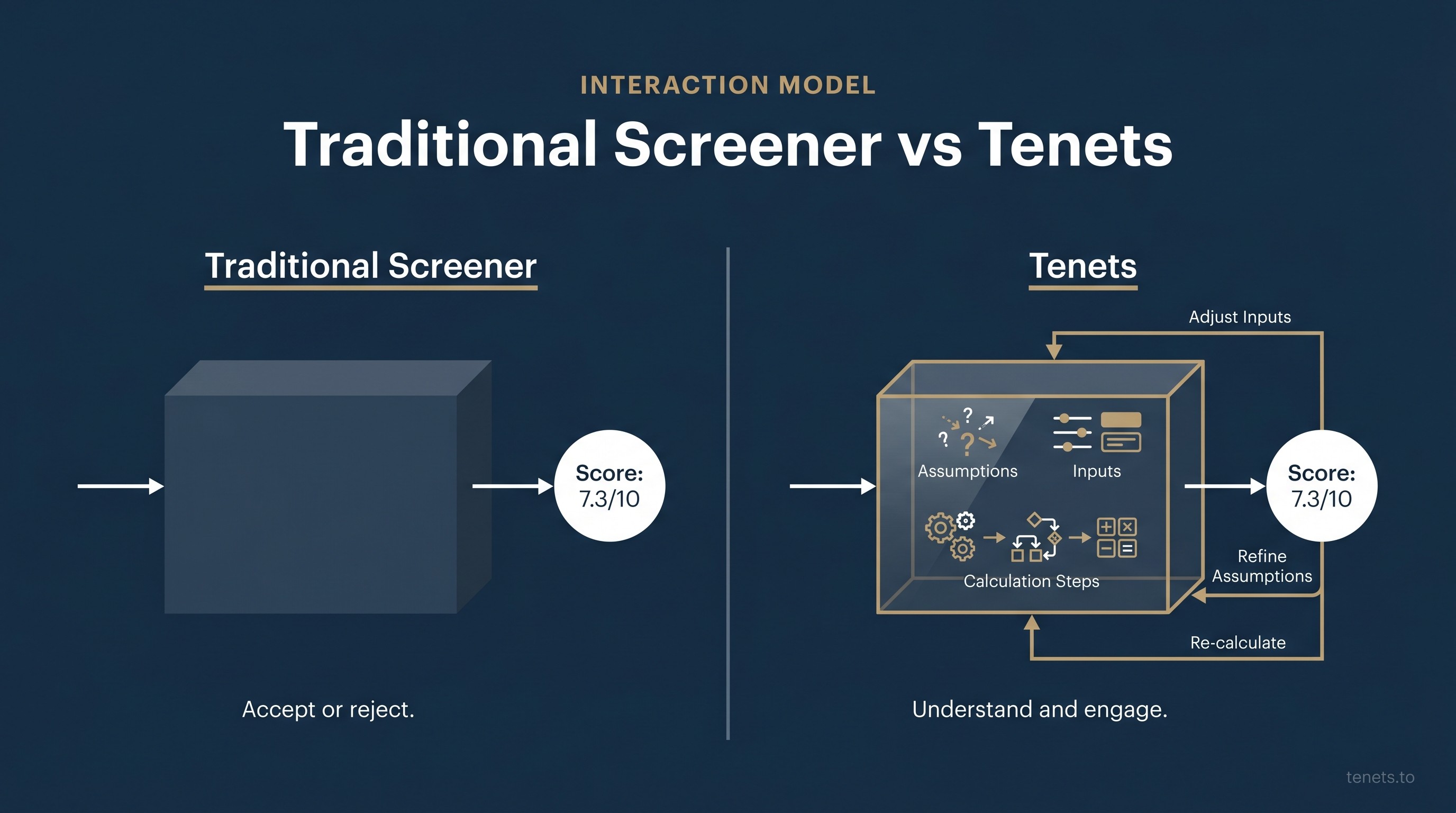

Every stock screener on the market gives you an answer. A score. A buy/sell/hold rating. A number out of ten. None of them show you the reasoning.

That gap, between the conclusions investing tools produce and the transparency investors need, is why Tenets exists. This post explains the philosophy behind the tool, the methodology decisions that define it, and why transparent reasoning matters more than any score.

Why traditional stock screeners fall short

Traditional stock screeners are designed around outputs. You enter your filters, the tool returns a list of stocks, and each one gets a score or rating. The implicit promise: trust the number.

The problem is not that the numbers are wrong. Many screeners use reasonable methodologies. The problem is that the numbers are opaque.

When Simply Wall St gives you a snowflake visualisation, you can see categories, value, future, past, health, dividend, but you cannot see the specific calculations driving each score. When Finviz shows you a stock's fundamentals, you get raw data points without a framework for synthesising them. When Koyfin gives you charts, the analytical interpretation is left entirely to you.

These are good tools. They serve real purposes. They all share the same structural limitation: the output is the product, and the reasoning behind that output stays hidden.

This matters because investing decisions are not maths problems with right answers. They are judgment calls built on assumptions. When you cannot see the assumptions, you cannot evaluate whether you agree with them.

Reasoning as the product

Paul Graham has a useful test for evaluating startup ideas: identify what everyone in an industry takes for granted, then ask what happens if the opposite is true.

In stock analysis tools, the universal assumption is that the answer is the product. The score. The recommendation. The rating. Every tool competes on producing a better answer.

We asked: what if the reasoning was the product?

Beyond the conclusion; the full calculation path. Every assumption made visible. Every input adjustable by the user. A system designed so that you can disagree with the method, not just the result.

This is a fundamentally different relationship between tool and user. Traditional screeners ask you to trust their judgment. Tenets asks you to engage with the methodology and form your own.

When we tested this approach, something unexpected happened. Users stopped asking "is this stock a buy?" and started asking "do I agree with this reasoning?" They adjusted inputs. They challenged assumptions. We want our users to treat the tool as a thinking partner rather than an oracle.

That shift, from consuming conclusions to engaging with reasoning, is what Tenets is designed to produce.

What is intangible-adjusted book value?

One of the first methodology decisions we made was to adjust book value for intangible assets.

In 1985, approximately 68% of S&P 500 market value was reflected in tangible assets on corporate balance sheets. By 2015, intangible assets represented 83% of total S&P 500 value. Today, that figure stands at 92%.

The implication is significant: traditional price-to-book ratios are comparing market prices against a number that misses the vast majority of economic value in modern companies.

R&D spending, brand building, software development, customer acquisition — under standard accounting rules, these expenditures are treated as expenses and written off immediately. They never appear as assets on the balance sheet, even though they represent the primary source of competitive advantage for most companies today.

Tenets uses Michael Mauboussin's framework for intangible-adjusted book value. R&D expenditures are capitalised and amortised over a five-year schedule, reflecting the typical productive life of research and development investments. SG&A expenditures, used as a proxy for brand and organisational capital, are capitalised and amortised over a three-year schedule.

This does not produce a perfect number. No adjustment can. It produces an honest number: one that reflects economic reality more accurately than raw book value. Because Tenets shows you the adjustment methodology, you can evaluate whether you agree with the amortisation periods, or whether you would use different assumptions for a specific company or industry.

A pharmaceutical company might warrant a longer R&D amortisation period. A fast-moving consumer brand might warrant a shorter SG&A period. The tool shows you the inputs; you decide whether to accept or adjust them.

For a deeper exploration of why traditional value metrics fail in an intangible economy, see our companion piece: Is Value Investing Dead? Why the Question Itself Is Wrong.

How Tenets combines quality and value

The single most common mistake in value investing is buying cheap stocks without quality filters. A stock trading at 6x earnings can be a bargain or a value trap. The difference is almost always quality.

Piotroski F-Score

Joseph Piotroski's F-Score is a nine-point checklist covering profitability, leverage, and operating efficiency. Each criterion is binary — pass or fail — producing a score from 0 to 9. The academic research is clear: high-F-Score stocks within the cheapest decile of the market have historically outperformed low-F-Score stocks in the same decile by a wide margin. Quality separates the bargains from the traps. Tenets calculates the F-Score for every stock and shows you each of the nine components individually, so you can see exactly which quality tests a company passes and fails.

The importance of quality filters came up at a UBS fireside chat in Omaha on May 1, 2026. Bill Ackman pointed out that even Buffett misidentified durable businesses — World Book Encyclopedia, newspapers — that were later disrupted. Ryan Israel, Pershing Square's CIO, added: "In a world where change is happening more rapidly, what are the things that won't be changing? That's a really big focus for us on capital allocation." Quality metrics function as the disruption filter that separates genuine bargains from value traps in an era of accelerating AI-driven change.

Novy-Marx gross profitability

Robert Novy-Marx's research demonstrated that gross profitability — gross profit scaled by total assets — is the quality signal that complements value most effectively. Profitable firms generate significantly higher returns than unprofitable firms, even after controlling for value. Gross profitability captures a company's fundamental pricing power and operational efficiency before management decisions about reinvestment, capital allocation, and financial engineering distort the picture.

Forward free cash flow yield

Tenets uses forward free cash flow yield, not trailing earnings, not book value, as its primary valuation anchor. It answers the most important question in valuation: what is the business expected to generate in actual cash, relative to what the market charges you to own it? Earnings can be manipulated through accounting choices. Book value misses intangibles.

Free cash flow, the cash a business generates after all reinvestment, is the closest thing to economic truth in financial analysis. By using forward estimates rather than trailing figures, Tenets captures the market's current expectations, which is where the real analytical work happens: deciding whether those expectations are too high, too low, or roughly right.

For complete methodology documentation, visit How Tenets Works.

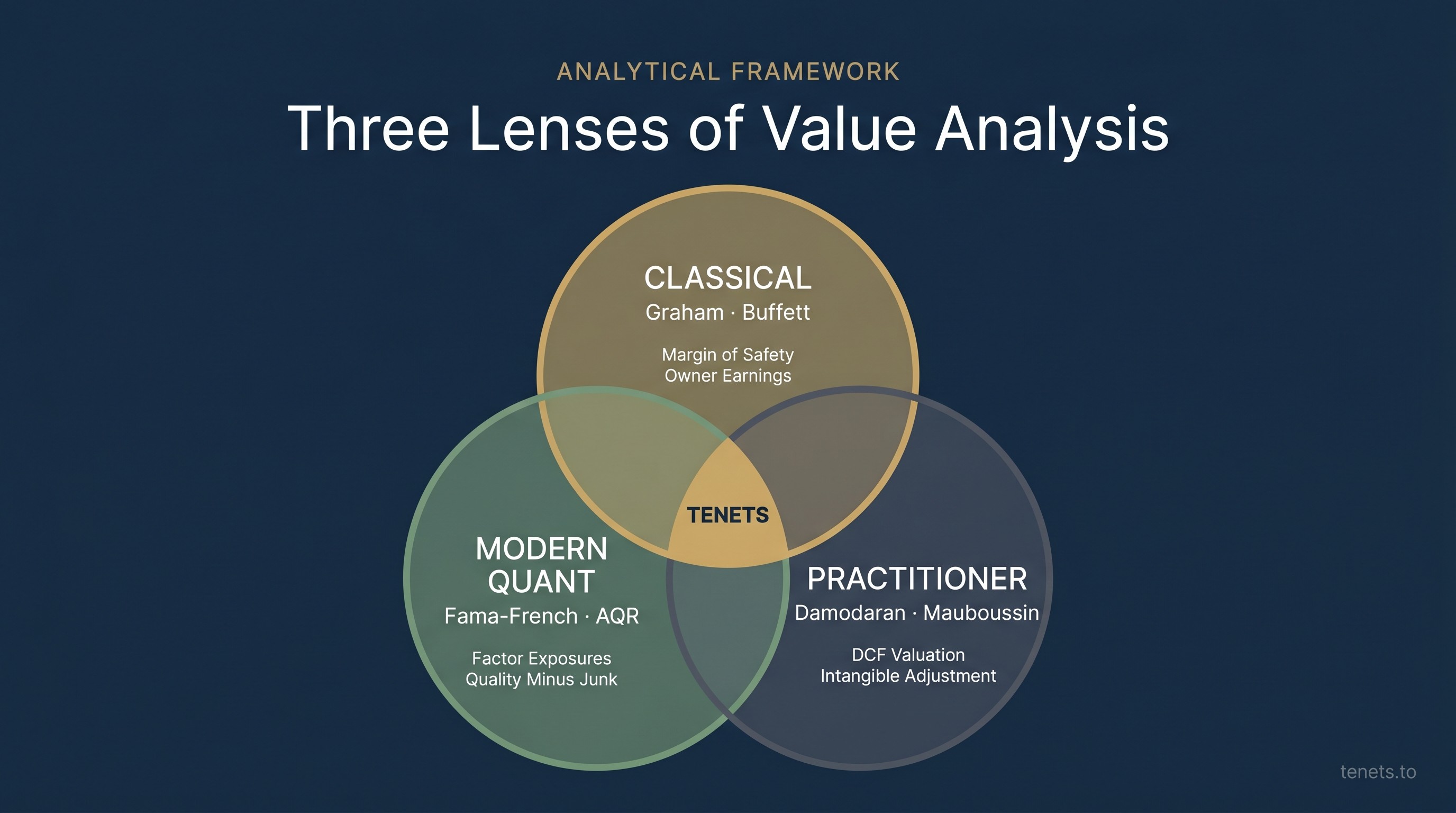

Three analytical lenses

Most investing tools serve a single school of thought. Tenets integrates three, because each lens catches things the others miss.

Classical (Graham and Buffett)

The margin of safety framework. What is the estimated gap between market price and intrinsic value? How much room for error exists before the investment thesis breaks? Classical analysis anchors you to the fundamental question: am I paying less than this business is worth? It provides discipline against overpaying, even for excellent businesses.

Modern quant (Fama-French, AQR, Piotroski)

Factor-based analysis. Where does this stock sit on the value, quality, size, and momentum spectrums? What do academic return predictors say about the expected return profile? Quantitative analysis provides statistical rigour and cross-sectional context. It answers: relative to the universe of stocks, where does this one sit on the dimensions that have historically predicted returns?

Practitioner (Damodaran, Mauboussin)

Real-world valuation frameworks. Damodaran's DCF approach. Mauboussin's intangible adjustments. The bridge between academic theory and practical application. Practitioner analysis forces you to make explicit forecasts, about revenue growth, margins, reinvestment rates, cost of capital, and shows you how sensitive the valuation is to each assumption.

Classical investors sometimes ignore factor exposures that predict returns. Quant models sometimes miss qualitative context that matters for individual stocks. Practitioner frameworks sometimes overfit to narratives. Tenets shows you all three perspectives. You choose which lens matters most for your specific decision. The tool does not choose for you.

''the S&P 500 has compressed from approximately 22x to 20x earnings in 2026 despite the index being up 6%, because earnings growth has accelerated to roughly 15% year-over-year.

Why "value vs. growth" is the wrong frame

Tenets does not sort stocks into "value" or "growth." This is a deliberate decision.

The value-versus-growth dichotomy is an artefact of style-box thinking popularised by Morningstar in the 1990s. It was useful for categorising mutual funds. It is misleading for analysing individual stocks.

Consider: when Alphabet traded at 17x earnings while growing revenue 20% annually, traditional style boxes classified it as a growth stock. An investor buying a dominant business at 17x earnings with 20% growth was making a classic value play, paying less than the business was worth, with a wide margin of safety on growth.

Tenets scores the gap between market price and estimated intrinsic value, regardless of style-box labels. A growth stock trading below intrinsic value gets a high score. A value stock trading above intrinsic value gets a low one. The label is irrelevant; the maths is what matters.

The market setup

The timing is worth noting, though Tenets was built on principles, not timing.

The value spread, the valuation gap between cheap and expensive stocks, currently sits at the 91st percentile historically. MSCI EAFE Value has returned over 43% in the past year. Headline multiples are also misleading: as Ryan Israel noted at the UBS fireside chat in Omaha, the S&P 500 has compressed from approximately 22x to 20x earnings in 2026 despite the index being up 6%, because earnings growth has accelerated to roughly 15% year-over-year. Bill Ackman went further: "I actually think the stock market may look cheap when we look back."

The version of value investing that died deserved to die. Buying low price-to-book stocks with no quality filter, no intangible adjustment, no forward-looking cash flow analysis: that strategy was broken by the economy's shift toward intangible-driven business models.

The version that adapted, accounting for intangibles, combining quality with cheapness, using forward cash flow instead of backward-looking book value, has rarely looked more attractive.

The question was never "is value investing dead?" The question was always "which version of value investing are you doing?"

Source(s)

UBS Wealth Management. "Value Investing in an Uncertain World: A Fireside Chat with Bill Ackman and Ryan Israel." UBS Events, May 1, 2026, Omaha, NE. https://www.ubs.com/us/en/wealth-management/insights/events/2026/value-investing-with-bill-ackman.html

Try Tenets

Tenets is built for investors who want to see the reasoning, not just the result.

Every assumption exposed. Every input adjustable. Three analytical lenses. Intangible-adjusted valuations. Quality and value combined.

Try Tenets free: Join 100+ investors on the waitinglist - launching soon.

Want the methodology deep dives and market analysis in your inbox? Subscribe to our newsletter.

Every Sunday evening, one company analysed like you always meant to. Safety screens. Quality checks. Valuation models. Every assumption visible. No black boxes.

Free. No spam. Unsubscribe anytime.